Salesforce slips after soft Q2 guidance despite earnings beat and AI driven growth

In this edition of Lens on Markets, we look into how Salesforce forecast second-quarter revenue, was below Wall Street expectations

Market Performance

South African Market Summary

South African equities softened yesterday, with the JSE All Share Index slipping 0.34% to 115,426.89 points and the Top 40 losing 0.42% to 107,510.04 points, as investors turned cautious ahead of the South African Reserve Bank’s policy decision. Economists polled by Reuters expect the central bank to raise interest rates by 25 basis points to 7.00%, from 6.75%, keeping monetary policy firmly in focus. Separately, the BRICS Business Council’s South African chapter began private-sector consultations to shape the country’s position ahead of the BRICS summit in India, amid debate over trade deficits and limited export diversification. Investor sentiment may also be affected by renewed concerns around anti-immigrant tensions following the voluntary repatriation of nearly 300 Ghanaian nationals.

European Market Summary

European equities ended broadly unchanged on Wednesday, with the STOXX 600 edging 0.03% higher to 628.18 points as gains in automobile and chemical shares offset concerns over the Iran war and its potential impact on energy markets. The index remained near pre-conflict record levels, trading about 1% below its all-time high reached before the war began in late February. The European Central Bank warned that the conflict and persistent trade tensions could weaken eurozone growth, lift borrowing costs and pressure public finances. ECB chief economist Philip Lane also cautioned that the energy shock may have a lasting inflationary impact, particularly if countries rebuild inventories or diversify energy supply. Meanwhile, UK auto production fell 1.2% year-on-year in April.

US Market Summary

US equities advanced on Wednesday, with the Dow Jones Industrial Average reaching a record closing high as healthcare and consumer shares provided support. The S&P 500 and Nasdaq also posted fractional gains, securing record closes for a second consecutive session, although momentum cooled as investors paused following the recent AI-led rally and monitored Middle East peace talks. Retail earnings helped sentiment, with Bath & Body Works jumping 9.7% after first-quarter sales and profit beat expectations, while Abercrombie & Fitch also gained after delivering a strong quarterly profit. Attention now turns to Thursday’s personal consumption expenditures inflation data, the Federal Reserve’s preferred price gauge, which could offer fresh direction on the monetary policy outlook under new chair Kevin Warsh.

Asian Market Summary

Asia-Pacific markets opened lower on Thursday as investors assessed mixed signals from Iran-US negotiations and the durability of a fragile ceasefire. In South Korea, the Bank of Korea left its benchmark interest rate unchanged at 2.50%, in line with expectations, although two of seven board members voted for a hike, signalling a more hawkish policy bias under new governor Shin Hyun Song. The central bank raised its 2026 inflation forecast to 2.7% from 2.2%, reflecting higher oil prices linked to the Iran war, while lifting its growth outlook to 2.6% from 2.0% after strong first-quarter expansion. Separately, South Korean exports are expected to rise for a 12th consecutive month in May, driven by AI-related chip demand.

Commodity Market Summary

Gold prices fell to a two-month low on Thursday as fresh US attacks on Iran strengthened the dollar, reduced the metal’s appeal and added uncertainty to the interest rate outlook. The escalation also pushed oil prices about 2% higher in early trade after reports of overnight US strikes on an Iranian military site, despite ongoing negotiations between Washington and Tehran aimed at ending the three-month conflict. Higher crude prices have renewed concerns that energy-driven inflation could prove more persistent, complicating the outlook for central banks and risk assets. In the United States, crude inventories fell by 2.8 million barrels last week, marking a sixth consecutive weekly decline, with official Energy Information Administration data due on Thursday.

Currency Market Summary

The South African rand was steady in early trade on Wednesday as investors assessed renewed geopolitical risks after Iran accused the United States of violating a fragile ceasefire near the Strait of Hormuz. The dollar held close to a one-week high on Thursday after reports of fresh US strikes on an Iranian military site, complicating peace talks between Washington and Tehran and supporting demand for the greenback. The dollar index was little changed at 99.288, near its strongest level since 22 May, while the yen weakened towards levels that recently prompted central bank intervention. Markets now turn to the core PCE deflator, the Federal Reserve’s preferred inflation measure, for further guidance on the US interest rate outlook.

Domestic Company News

Reinet Investments S.C.A. (RNI) -11.14%

Reinet Investments reported a 4.5% decline in net asset value for the year ended 31 March 2026, falling by EUR314 million to EUR6.6 billion from EUR6.92 billion a year earlier. Net asset value per share decreased to EUR36.31 from EUR38.04, although the group has still delivered compound annual NAV growth of 8.3% in euro terms since March 2009, including dividends paid. During the year, Reinet made EUR306 million of commitments to new and existing investments, with EUR109 million funded. The group received EUR303 million in ordinary and special dividends from Pension Insurance Corporation and subsequently sold its entire holding to Athora for about EUR3.3 billion. Reinet proposed a dividend of EUR0.435 per share, up 17.6%.

Telkom SA SOC Limited (TKG) +12.02%

Telkom expects a stronger full-year performance for the year ended 31 March 2026, supported by its data-led strategy, improved operating profitability and continued balance sheet repair. Basic earnings per share from continuing operations are expected to rise 20% to 30% to between 679.2 cents and 735.8 cents, compared with 566.0 cents a year earlier. Headline earnings per share are forecast to increase 45% to 55% to between 677.9 cents and 724.6 cents, from 467.5 cents previously. Earnings growth was driven by solid underlying operations, structural cost optimisation and lower finance charges following reduced debt. The prior year was affected by once-off retirement fund derecognition and restructuring costs, while property disposal gains were lower in the current year.

Sygnia Limited (SYG) +2.85%

Sygnia expects a stronger interim earnings performance for the six months ended 31 March 2026, with headline earnings per share forecast to increase by between 20.0% and 25.0%. HEPS is expected to rise to between 135.8 cents and 141.5 cents, compared with 113.2 cents for the prior corresponding period. Diluted headline earnings per share are also expected to increase by between 20.0% and 25.0%, to between 134.3 cents and 139.9 cents, from 111.9 cents a year earlier. The trading statement indicates continued earnings momentum from the asset management group, although the financial information has not been audited, reviewed or reported on by external auditors. Sygnia expects to release its full interim results on or about 8 June 2026.

Emira Property Fund Limited (EMI) -3.56%

Emira Property Fund reported a resilient distribution performance for the year ended 31 March 2026, despite weaker portfolio revenue and lower earnings. Distributable income increased to R648.1 million from R642.2 million, while distributable income per share rose 3.7% to 129.53 cents. The board declared a final dividend of 64.61 cents per share, taking the total dividend for the year to 129.01 cents, up 4.1% from 123.89 cents in the prior year. Directly held portfolio revenue declined 15.7% to R1.46 billion, while headline earnings per share fell 58.2% to 160.74 cents and earnings per share decreased 68.7% to 154.35 cents. Net asset value per share improved 1.3% to 2 094.9 cents, offering some reported balance to the weaker income statement metrics.

Global Company News

HP Inc. (HPQ) +4.34%

HP beat second-quarter expectations as demand for AI-optimised personal computers supported revenue growth, although management warned that rising memory costs would pressure margins. Revenue for the quarter ended 30 April increased 9% year-on-year to US$14.41 billion, ahead of analyst expectations of US$14.07 billion, while adjusted earnings of US$0.86 per share exceeded forecasts of US$0.71. AI PCs accounted for 44% of total PC shipments, up from more than 35% in the previous quarter, and are expected to reach 60% to 70% next fiscal year. HP is responding to memory-chip shortages through product reconfiguration, cheaper sourcing, pricing adjustments and a focus on premium categories. The company narrowed its fiscal 2026 adjusted EPS outlook to US$2.90-US$3.10, signalling cautious near-term margin expectations ahead.

Salesforce Inc. (CRM) -0.88%

Salesforce forecast second-quarter revenue, was below Wall Street expectations as concerns over AI-driven disruption to traditional software demand overshadowed a stronger first-quarter performance. The business software group expects second-quarter revenue of US$11.27 billion to US$11.35 billion, slightly below analyst forecasts of US$11.36 billion, while shares were marginally weaker in volatile after-hours trade. Investor sentiment remains pressured by fears that advanced AI tools could reduce demand for traditional software-as-a-service products, contributing to a sharp decline in Salesforce’s share price this year. However, first-quarter revenue rose to US$11.13 billion, ahead of expectations of US$11.05 billion, supported by adoption of AI-powered software. Adjusted earnings of US$3.88 per share beat forecasts of US$3.12, while subscription and support revenue grew 14% during the reported first quarter.

Click here for the daily moves of shares, indices and currencies.

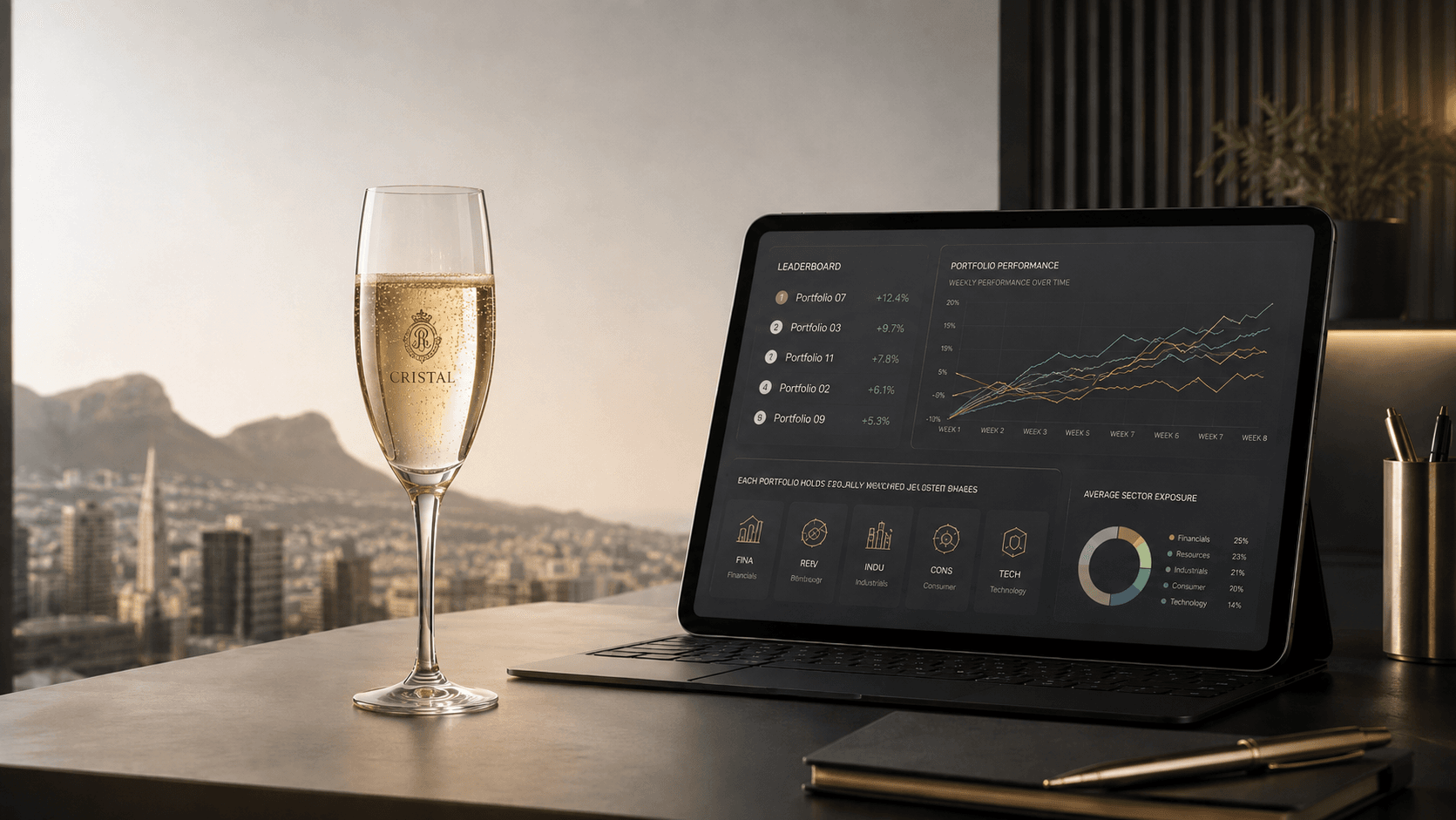

Cristal Challenge 2026 Leaderboard as at 3 July 2026

The premier stock-picking competition designed to engage, educate, and excite both novice and experienced investors.

Read more